By Kayla Villena, Senior Beauty Analyst, Euromonitor International

Clean beauty and conscious beauty were already gaining ground before the pandemic. A lack of standardization and trust in natural and organic labels and social and digital trends are driving these beauty segments. Digital platforms, in particular, created more discerning, empowered and knowledgeable consumers. Demographic shifts are also propelling the clean beauty trend. Younger generations express stronger interest in green, clean and conscious product attributes.

While there are various interpretations of clean beauty, this segment generally takes a minimalistic, simplistic and safety approach regardless of ingredient provenance. The fall of talcum powder is a prime example of clean beauty’s momentum in the U.S. Product usage concerns escalated when medically supported links to certain cancers and high-profile class action lawsuits surfaced, resulting in the cease of Johnson & Johnson’s talcum baby powder sales in the U.S.

COVID-19 is amplifying preventative health and safety priorities among consumers. Demand for natural or clean beauty and personal care products is at an all-time high. Immunity-boosting attributes are having a halo effect on beauty and personal care since popular ingredients like ginseng and turmeric have positive connotations in skin care. Additionally, the current events of racial injustice in the U.S. are having a ripple effect on broader beauty discussions around inclusivity, diversity and self-acceptance. In June 2020, Johnson & Johnson announced that the company would stop selling their Neutrogena Fine Fairness line in Asia Pacific and the Middle East and Clean & Clear Fairness line in India amid changing public sentiment on beauty standards.

The historically fast-growing beauty and personal care industry is influencing ingredient safety in consumer health, namely dermatologicals. Dermatologicals, such as antiparasitics/lice and hemorrhoid treatments, have different purchasing motivations and positionings than anti-agers and toners. These treatments are curative—used to solve an already-existing problem—whereas skin care is used for both preventative and solution-based benefits. Despite the different purchase motivations, both categories highlight the importance of skin health and overall wellness in the U.S.

Clean label claims overlap in U.S. skin care and dermatologicals, suggesting synergies

Euromonitor International extracted data of stock keeping units (SKUs) from more than 1,500 online retailers to track 150 product claims in 11 industries across 40 countries. The Product Claims and Positioning system can be used to understand trending claims, share of product claims in a given category and brand positioning across dietary, ethical and clean labels.

No parabens, natural, fragrance-free and no phthalates were the top-four clean labels claims, respectively, in skin care and dermatologicals in the U.S. last year, according to Euromonitor International. Across these four claims, skin care had higher penetration than dermatologicals, suggesting that clean labels in skin care not only overlap but influence claims in dermatologicals despite different purchasing motivations.

Slight differences following the top-four claims identify nuances and innovation opportunities across categories. For example, no silicone is a trending claim in skin care due to pore-clogging concerns; however, no silicone does not appear as a claim in dermatologicals. The convergence between health and beauty will only accelerate. Identifying overlapping claims from adjacent categories and analyzing product positioning helps players looking to expand.

Source: Euromonitor International

Source: Euromonitor International

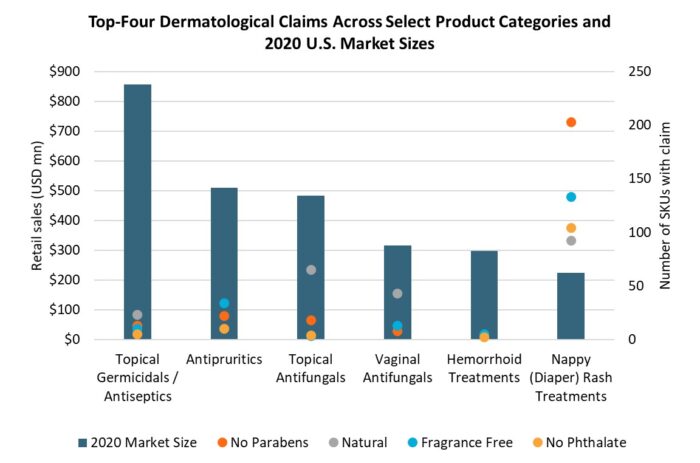

Identifying clean label opportunities and penetration in skin care and dermatologicals

Over the past decade, demand for optimal efficacy and functionality propelled innovation and new product development within beauty and personal care. Several brands tap into medical or pharmaceutical heritage to meet these consumer expectations. As a result, beauty brands in the U.S. have also crossed over into the dermatological space to expand customer reach. Direct-to-consumer brands, such as Hims, Hers and Keeps, are notable success stories that straddle both industries with a portfolio that features hair loss treatments as well as beauty products. Understanding the leading dermatological claims will help existing brands innovate and beauty players identify areas to explore.

Source: Euromonitor International

Source: Euromonitor International

Note: 2020 market sizes are preliminary. Top-four claim selection based on the number of SKUs with claim at dermatological category level.

Topical germicidals and antiseptics generate the most sales of dermatological categories in the U.S. However, the number of topical germicidal and antiseptic SKUs carrying a leading clean label claim from the broader dermatological category is notably lower than diaper rash treatments, which is the sixth largest category in retail sales, according to Euromonitor International. Baby and child-specific products experienced a wave of premiumization that coincided with the first-wave naturals movement due to ingredient-savvy parents concerned about the safety of baby products. As a result, clean label claims heavily influence the positioning of diaper rash treatments, and this level of influence does not currently exist for other dermatological categories. In contrast, the top claims in topical germicidals and antiseptics are all clean label, but the lower number of SKUs tagged suggests that other factors, such as efficacy, drive the category.

Clean label claims also have potential in hair loss treatments, which was the fastest-growing dermatological category in the U.S. in 2020, according to Euromonitor International. Natural direct-to-consumer brands that come from a non-pharmaceutical heritage were a key growth driver for this segment.

Source: Euromonitor International

Source: Euromonitor International

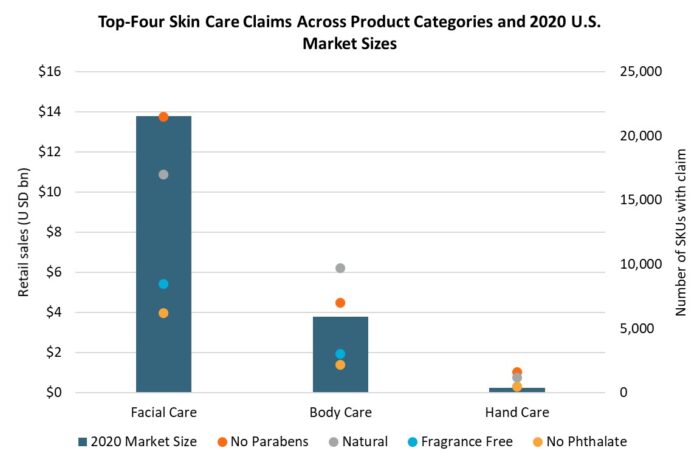

Note: 2020 market sizes are forecasts. Top-four claim selection based on the number of SKUs with claim at skin care category level.

The number of SKUs tagged with a leading skin care clean label claim trended relative to product-level sales. Looking at the leading clean label claims provides insight on the nuances between product categories, even though all are applied to the skin. For example, organic is the second-leading clean label claim in body care but ranks fourth in facial care and hand care, suggesting that an organic claim may be more salient in body care positioning than other skin care products.

Looking forward: Battle between efficacy and clean positioning intensifies as COVID-19 pandemic spotlights the importance of proven, science-based claims

During the pandemic, simple, minimalistic, back-to-basics claims that also emphasize ingredient safety will resonate among U.S. consumers. Efficacy is paramount as consumers’ skin undergoes new stresses, such as mask wearing. Restricted discretionary spending, due to lockdown mandates, is expected and suggests that consumers are reluctant to purchase skin care or dermatologicals that do not achieve claimed results. Clean beauty claims ultimately feed into the concept of skin health and wellness, which will be magnified post-COVID-19. Health, beauty and personal care players should look to each other for inspiration and innovation as product distinctions continue to merge.

About Euromonitor International

Euromonitor International is a global market research company providing strategic intelligence on industries, companies, economies and consumers around the world. Comprehensive international coverage and insights across consumer goods, business-to-business and service industries make our research an essential resource for businesses of all sizes.

About Kayla Villena

Kayla Villena is a senior analyst at Euromonitor International based in Chicago. She analyses the beauty and personal care industry, looking at changing consumer preferences, megatrends influencing adjacent industries, and the ripple effects from industry disruptors and innovators. Leveraging custom consulting experience at Euromonitor, she works closely with stakeholders to understand their strategic goals and communicate how to win, synthesizing beauty insights with Euromonitor’s retailing and digital consumer systems, as well as Euromonitor’s Beauty Survey and Via Pricing systems.

Kayla Villena is a senior analyst at Euromonitor International based in Chicago. She analyses the beauty and personal care industry, looking at changing consumer preferences, megatrends influencing adjacent industries, and the ripple effects from industry disruptors and innovators. Leveraging custom consulting experience at Euromonitor, she works closely with stakeholders to understand their strategic goals and communicate how to win, synthesizing beauty insights with Euromonitor’s retailing and digital consumer systems, as well as Euromonitor’s Beauty Survey and Via Pricing systems.

She has spoken at industry events, such as in-cosmetics North America, Cosmoprof North America, MakeUp in New York, and several Jefferies’ events. She is a regular contributor to Natural Products INSIDER and Beauty Packaging and has been featured in Bloomberg, The Wall Street Journal, CosmeticsDesign and Glossy, among other publications.

Kayla holds master’s and bachelor’s degrees in communication from the University of Florida.

Categorized in: Trends/Insights